If the Chancellor does cut the Cash ISA allowance on 26 November, many savers will cry foul. Yet this may be one of the more rational pieces of policymaking the UK has seen in recent years. For too long, savers have been sheltering cash from tax, not from inflation. And it’s inflation – not income tax – that is quietly dismantling their wealth.

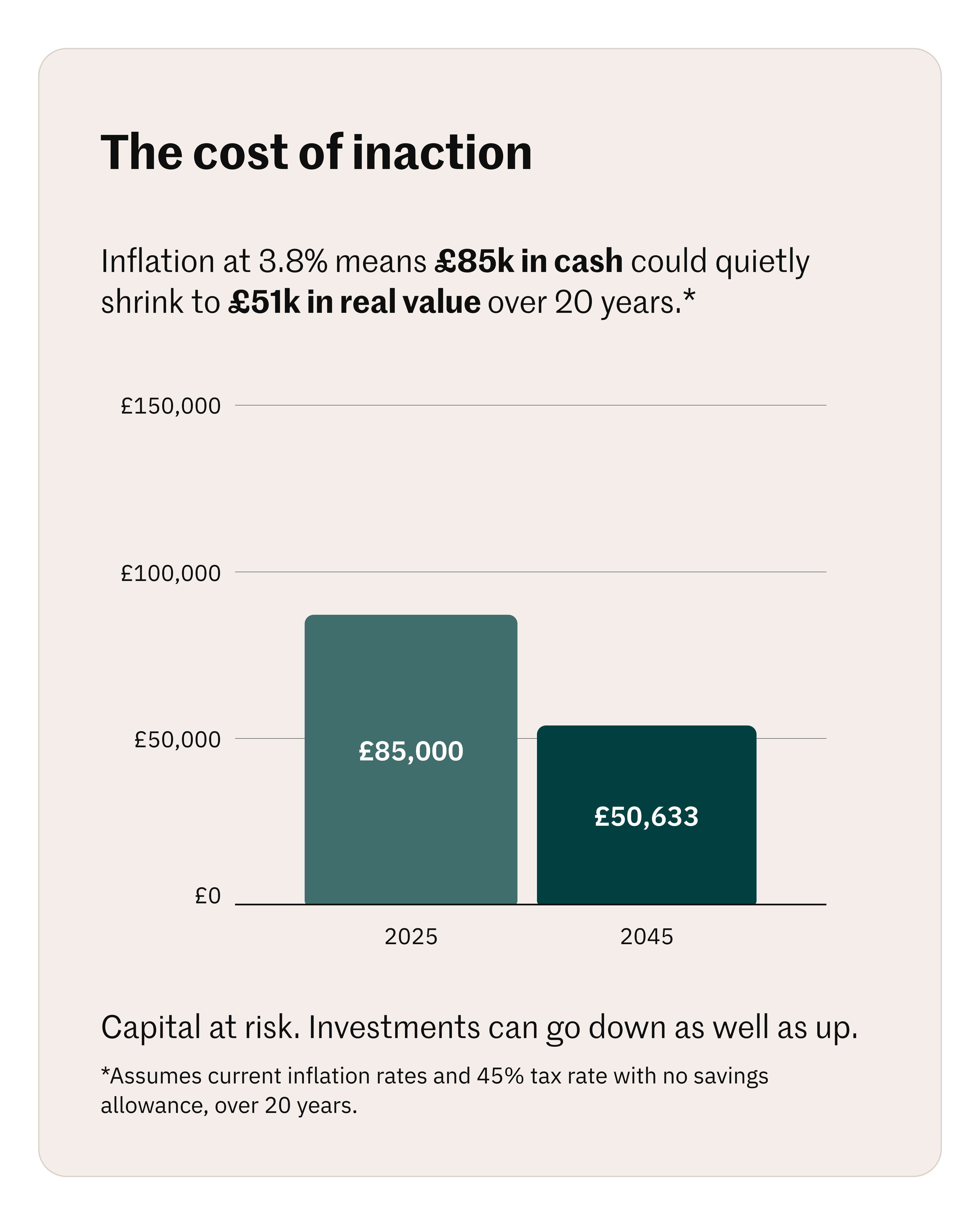

The numbers speak louder than any Budget speech. At today’s average savings rate of just 2.26%, an £85,000 cash balance steadily loses ground. Over 20 years, factoring in inflation and higher-rate taxation, that pot could shrink in real terms to just £50,633 – a staggering 40% erosion in purchasing power, without a single tax hike.

By contrast, investing that same amount with an assumed 7% annual return – even after capital gains tax and fees – could preserve or grow your wealth significantly. In a General Investment Account (GIA), it could be worth £128,583 in today’s money – a 51% real increase.

Redirecting allowances away from Cash ISAs and toward Stocks & Shares ISAs would not necessarily constitute government overreach; it could be seen as a long-overdue course correction. The UK’s historic preference for cash and property has often kept capital tied up in low-growth assets. Encouraging participation in global markets is a mathematical rather than ideological choice.

As of now, we can of course only speculate. None of these ideas have been confirmed, and any forward-looking assessments are based on current trends and hypothetical changes.

The end of 'my home is my pension'?

Those born between approximately 1965 and 1980 – Gen X – face a more existential challenge.

Many have most of their wealth in property and pensions, both now in the Treasury’s crosshairs. With discussions around replacing stamp duty with property taxes, or extending capital gains to main residences, the 'my home is my pension' mantra may soon prove outdated. Diversification will be the cornerstone of financial resilience in the coming decade.

And then there’s the matter of fees; the silent partner of inflation. A 2-3% annual wealth management charge, still common in traditional setups, can quietly erase half a portfolio’s real growth over twenty years. Combine this with inflation and frozen tax thresholds, and even solid market returns may struggle to outpace erosion.

The truth is simple but uncomfortable: investors fear policy change, yet inaction can be the greater threat to wealth. The most significant risk rarely stems from a Budget announcement; it’s the slow, compounding damage of capital that sits idle, is over-concentrated, or burdened by high costs.

The Chancellor may well tinker with thresholds and allowances. But in the meantime, financial resilience begins with strategic, inflation-aware, and cost-effective decisions made today.

Don't let your money stand still

If you haven't opened or funded your Prosper investment account, now is the time to act. Choose from our personal pension (SIPP), flexible Stocks & Shares ISA, and/or GIA and start maximising your potential wealth with low to zero fees.

Capital at risk. Investments can go down as well as up. Uninvested cash doesn't earn interest.

We don’t currently offer annuities or drawdown support, including for those who have already taken withdrawals from a pension, but we’re working on adding these options.