In the high-stakes world of investment, risk is a familiar adversary. Volatility, market cycles and macroeconomic uncertainty are regularly scrutinised. But there’s a quieter, more predictable force undermining your wealth. One rarely acknowledged with the urgency it deserves.

It’s not the market. It’s the model. And it comes dressed as fees.

The silent compounding effect

Consider a conservative scenario: a £250,000 portfolio growing at 5% annually over 30 years. That’s a reasonable horizon for professionals, entrepreneurs, or families planning for succession.

Now compare the outcomes under different fee structures (including annual platform and fund fees):

- 2% fees: £848,040

- 0.42% fees (UK platform average): £1,205,193

- 0% fees: £1,330,486

The result? Nearly half a million pounds in lost value between the highest and lowest-cost options.

This isn’t volatility. It’s arithmetic.

What are you really paying for?

Fees were once the cost of access; gatekeepers to markets, managers and expertise.

Yet even as low-cost ETFs, algorithmic trading and regulatory transparency have shifted the economics of investing, many investors still find themselves paying platform fees just to hold assets; management fees, particularly on active funds; trading costs for simple transactions; or exit fees to leave outdated platforms.

These may seem individually modest, but they are collectively corrosive.

Fee efficiency: The new frontier of smart investing

Wealth isn’t just built through smart bets and good timing. It’s preserved through intelligent structuring.

Fee discipline – like tax optimisation or diversification – can have a significant compounding effect over time. It’s not about avoiding all fees; it’s about eliminating those that add cost without delivering equivalent value.

And for high-net-worth individuals with long horizons, that distinction matters more than ever.

A new breed of platform

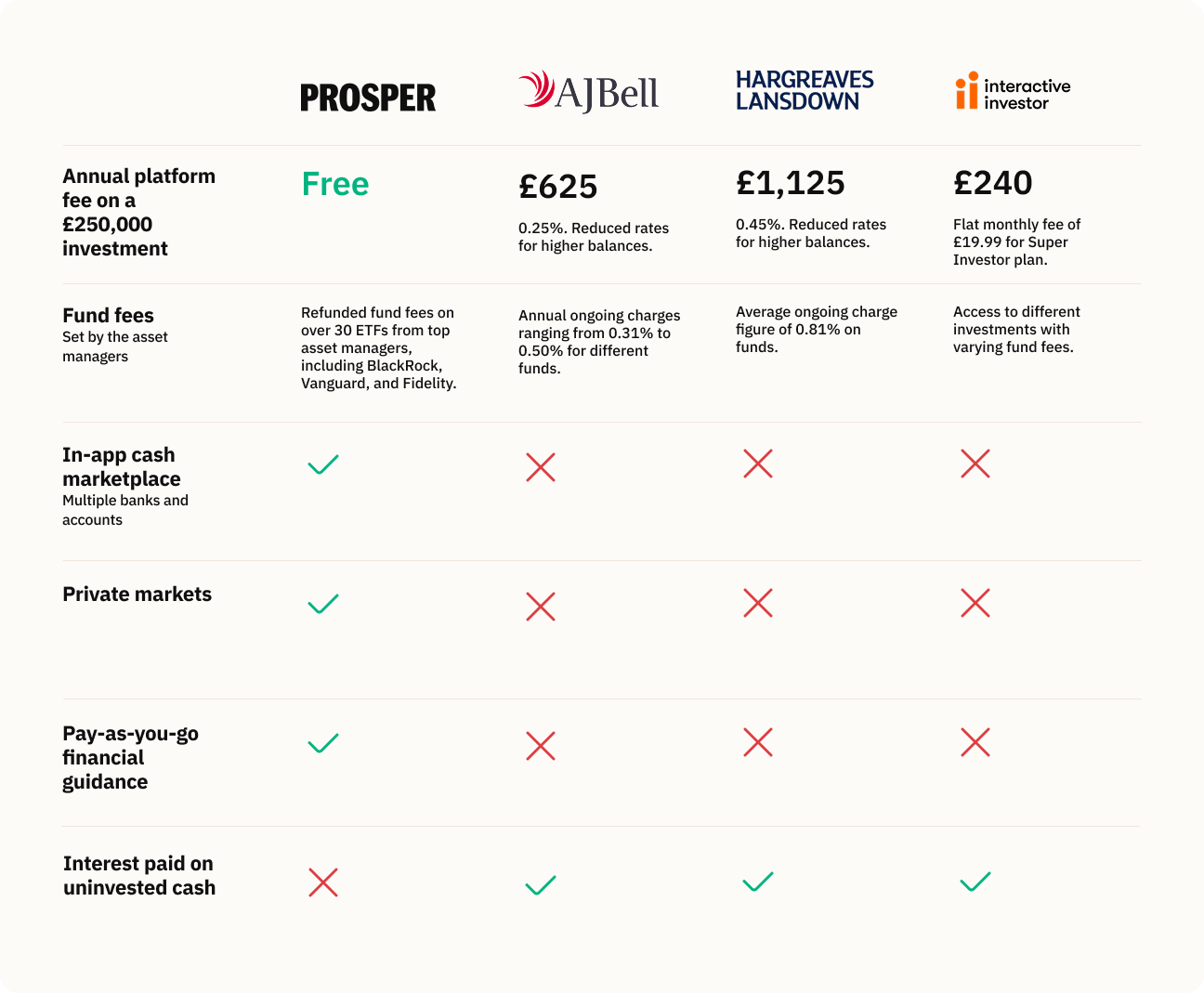

A number of innovative financial services are emerging that challenge the traditional model. One such example is Prosper, a UK-based wealth platform designed with cost efficiency and transparency at its core.

Unlike conventional platforms that layer on charges, Prosper minimises them, to the point of making zero-fee investing a practical reality. It charges no platform, transaction, transfer, or exit fees, and goes further by refunding fund management charges on more than 30 widely held ETFs from global asset managers like BlackRock, Vanguard and Fidelity.

You should bear in mind that the value of investments may rise or fall, meaning you may receive back less than the amount you initially invested.

Investors can access over 200 funds and more than 50 FSCS-protected UK bank savings products, with all holdings visible through a single, integrated app. For those seeking broader exposure, Prosper also offers optional access to private markets for eligible clients, alongside pay-as-you-go financial guidance, with an AI-powered guidance service on the horizon.

This is not just cost-cutting for its own sake. It represents a structural rethink built for financially literate investors who prioritise clarity, control and long-term performance over legacy frictions.

It’s worth noting, however, that your capital is at risk when you invest. Private market investments are particularly high risk and only available to high-net-worth and professional investors. Don’t invest unless you’re prepared to lose all the money you invest. If you’re unsure about investing, you should speak to an independent financial adviser before proceeding.

Clarity over complexity

A natural question arises: how can a platform so lean remain financially viable?

Prosper retains interest earned on uninvested cash held within its investment accounts and ‘wallet’, a practice it discloses transparently. Unlike other providers, however, this mechanism is designed not to reward inactivity, but to encourage capital to be invested rather than sitting idle.

Incentives are therefore aligned. Prosper performs better when your portfolio does; not by charging more, but by helping you keep more of what you earn.

As the platform grows, it plans to introduce new services with the same philosophy: fair, transparent pricing with no hidden costs. But the core Prosper experience remains unchanged: low-cost, clear and uncompromisingly investor-first.

Sources: Prosper, AJ Bell, Hargreaves Lansdown, interactive investor, Unbiased.

Investments can go down as well as up.

Not for everyone – and that’s the point

Traditional wealth managers aren’t obsolete. For clients who want hands-on advice and white-glove service, they still serve a purpose. But for affluent investors who like to make decisions with a tech-first approach, Prosper represents a new breed.

Increasingly, investors and savers are asking for a platform that doesn’t get in their way, with a human face to back it up. Prosper is unusual in offering human customer support that’s based in the UK as well as instant messaging from its trained in-app AI agent for straightforward requests.

Final thoughts: Sophistication isn’t complexity, it’s efficiency

Wealth creation has always been part art, part science. But in today’s landscape, structural efficiency is no longer optional, it’s essential.

In a low-growth, high-fee world, every hidden cost becomes magnified. Platforms that offer alignment, simplicity and transparent pricing will lead the next phase of wealth management.

This isn’t about rejecting advice or sacrificing strategy. It’s about reclaiming control and demanding a model where more of your wealth stays where it belongs. With you.

Capital at risk. Investments can go down as well as up. Prosper does not offer investment advice. If you are unsure about investing, please speak to an independent financial adviser before proceeding. Prosper Savings Limited is authorised and regulated by the Financial Conduct Authority (FCA), registration number 991710.